Bitcoin income strategies based on covered call and secured put selling have attracted significant institutional assets over the past year. These strategies generate consistent premium income in calm markets. In bitcoin, one volatility event can erase years of collected premium in a single month.

Using Two Prime's own modeling data across multiple market cycles, this article shows what these strategies actually produce and why the current volatility environment is particularly dangerous for new entrants.

By Alexander S. Blume

Co-Founder and CEO of Two Prime

The Appeal and the Trap

Over the past year, as bitcoin institutionalization has accelerated, we’ve seen a slew of income strategies on bitcoin enter the market, largely involving secured put and covered call selling, including offerings from Grayscale and BlackRock, to name a few. Some public companies with bitcoin holdings have also publicized their call and put selling programs to demonstrate how they monetize their holdings.

As AQR and many others have shown over the years, these strategies typically lose money over time. You are being paid to sell volatility. In bitcoin, this will eventually catch up to you. However, due to their simplicity, these products can be easily marketed, but they are, generally, poor performers, and, specifically for bitcoin, even worse!

Why This Moment Is Particularly Dangerous

These strategies often appear to work very well for short- and medium-term horizons, as they sell the volatility tails of an asset’s distribution curve to make money. Especially because bitcoin has no risk-free rate or native yield, methods of earning income on the asset require greater risk-taking. This is classic “penny in front of the steam roller” trading. You can pick up a few basis points each month, but volatility expansion can destroy years of returns in a single day.

It’s a particularly dangerous time for these strategies for three reasons:

The past six months of a gradual decline in BTC price and implied volatility have made these strategies work quite well, potentially leading groups to overestimate their long-term viability.

The compression of volatility over the past year means a sudden breakout is likely. We saw this happen this past week, with implied volatility moving from the 30s to the 90s in just a few days.

Bitcoin is a highly volatile asset.

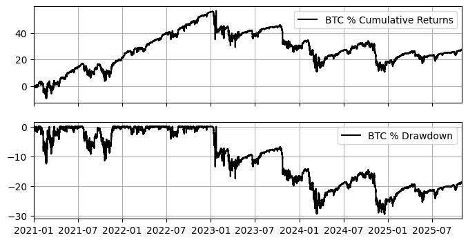

What the Models Show

Let’s look below at how these strategies have actually performed. Below is a model for selling monthly 10% out-of-the-money calls with 10% of one’s total BTC balance. Before any management fees, trading fees, or taxes, you can see that since 2023, call selling on bitcoin has been a net loser of BTC, to the tune of about 20% losses. This results from sharp price increases that force you to sell BTC when it’s going up. It is true that from 2021 to 2023, the strategy performed very well. This is the danger of these strategies. They look good for a while, then they don’t.

Covered call selling strategies have periods of strong performance, but can lose much of the return quickly.

Similarly, below is a model for selling monthly 10% out-of-the-money puts with 10% of one’s total BTC balance. Before fees and taxes, this strategy has performed poorly, losing up to 46% of total BTC in 2022. It has performed better in recent years, but is down over the full look-back period.

Who These Strategies Actually Serve

Ultimately, the efficacy of these strategies depends on your goals. If you are not interested in accumulating more bitcoin, selling calls or puts may make sense for you. If your goal is to accumulate more BTC, then these approaches will not serve you over time. They are good for companies selling them because they appear rational and can be sold easily, but ultimately do not align with most investors’ goals.

The real opportunity in bitcoin lies in leveraging arbitrage across fragmented infrastructure. The exchange, custodian, and prime broker complex has not fully consolidated. Those who can bridge the gaps stand to gain.

This article originally appeared in Forbes.